Investments, 12th Edition

Zvi Bodie, Alex Kane and Alan J. Marcus

ISBN:9781260571158

Investments, 12th Edition sets the standard as a graduate (MBA) text intended primarily for courses in investment analysis. The guiding principle has been to present the material in a framework that is organized by a central core of consistent fundamental principles and to introduce students to major issues currently of concern to all investors.

In an effort to link theory to practice, the authors make their approach consistent with that of the CFA Institute with many features consistent with and relevant to the CFA curriculum. By combining these principles and features, this title will enable you to deliver a sucessful course in which your learners are fully equipped with investments knowledge and practice.

What's new

Updated and Expanded Discussion Materials

Surrounding historical evidence on risk-return relation, extensions to the CAPM and recently uncovered market anomalies, for example, related to volatility, accruals, growth, and profitability.

New Words from the Street Content

Updated short articles and excerpts from periodicals such as The Wall Street Journal helping to bring the subject to life for learners.

Thoroughly Amended and New Content

Includes Fintech and cryptocurrency, updated material on the LIBOR scandal and a discussion of Schiller’s CAPE (cyclically-adjusted P/E ratio).

| PART 1: Introduction | PART 4: Fixed-Income Securities | |

| Ch. 1 The Investment Environment | Ch. 14 Bond Prices and Yields | |

| Ch. 2 Asset Classes and Financial Instruments | Ch. 15 The Term Structure of Interest Rates | |

| Ch. 3 How Securities Are Traded | Ch. 16 Managing Bond Portfolios | |

| Ch. 4 Mutual Funds and Other Investment Companies | ||

| PART 5: Security Analysis | ||

| PART 2: Portfolio Theory and Practice | Ch. 17 Macroeconomic and Industry Analysis | |

| Ch. 5 Risk, Return, and the Historical Record | Ch. 18 Equity Valuation Models | |

| Ch. 6 Capital Allocation to Risky Assets | Ch. 19 Financial Statement Analysis | |

| Ch. 7 Efficient Diversification | ||

| Ch. 8 Index Models | PART 6: Options, Futures, and Other Derivatives | |

| Ch. 20 Options Markets: Introduction | ||

| PART 3: Equilibrium in Capital Markets | Ch. 21 Option Valuation | |

| Ch. 9 The Capital Asset Pricing Model | Ch. 22 Futures Markets | |

| Ch. 10 Arbitrage Pricing Theory and Multifactor Models of Risk and Return | Ch. 23 Futures, Swaps, and Risk Management | |

| Ch. 11 The Efficient Market Hypothesis | ||

| Ch. 12 Behavioral Finance and Technical Analysis | PART 7: Applied Portfolio Management | |

| Ch. 13 Empirical Evidence on Security Returns | Ch. 24 Portfolio Performance Evaluation | |

| Ch. 25 International Diversification | ||

| Ch. 26 Hedge Funds | ||

| Ch. 27 The Theory of Active Portfolio Management | ||

| Ch. 28 Investment Policy and the Framework of the CFA Institute | ||

- Chapter 1: The Investment Environment - This chapter now addresses Fintech and cryptocurrency.

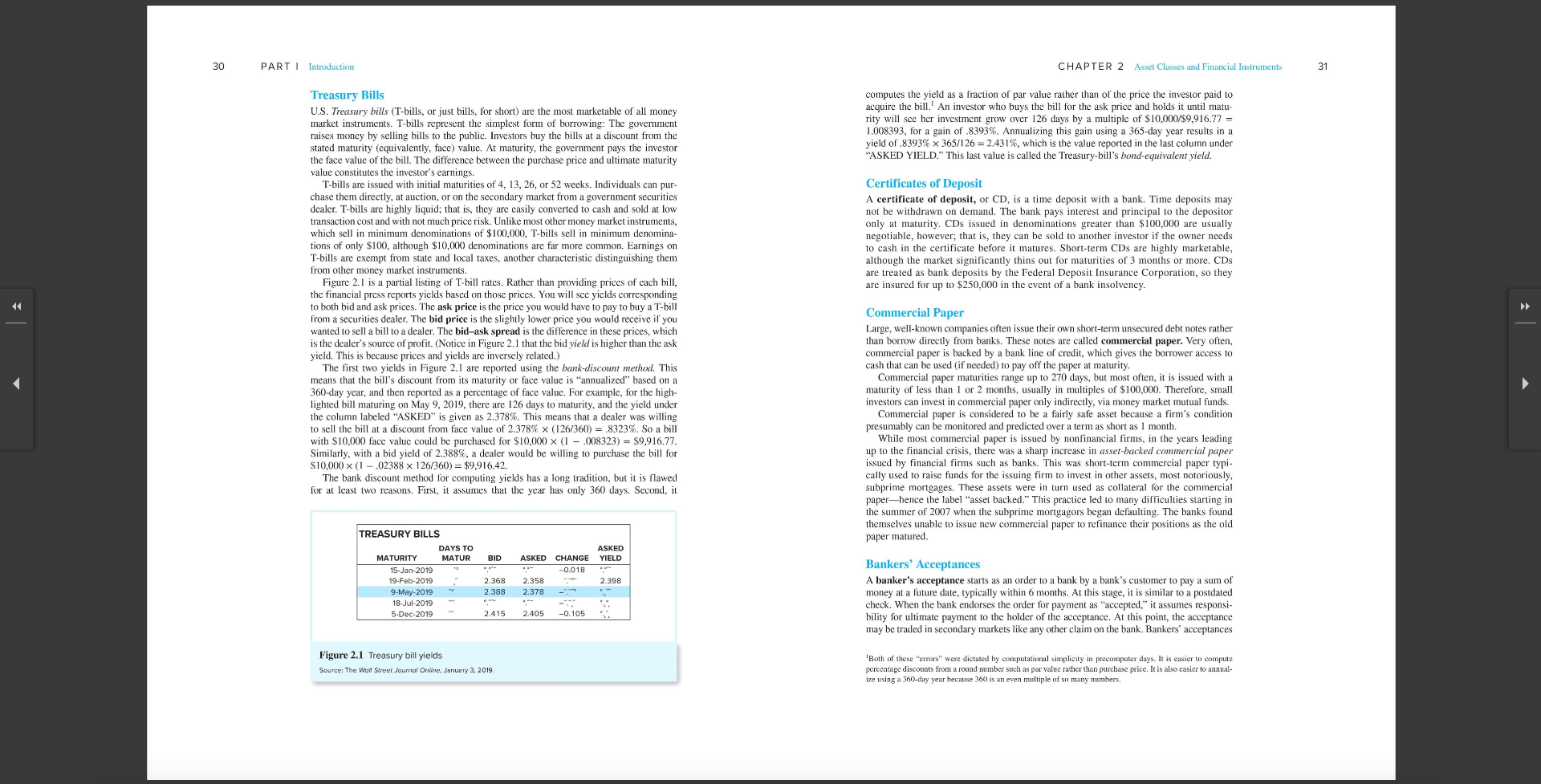

- Chapter 2: Asset Classes and Financial Instruments - The material on the LIBOR scandal and proposed replacements for the LIBOR rate that may be implemented in the next few years has been updated.

- Chapter 3: How Securities Are Traded - Updated for developments in market microstructure, including the replacement of specialists by designated market makers.

- Chapter 5: Risk, Return, and the Historical Record - Extensively reorganized and substantially streamlined. The material on interest rates and the discussion of historical evidence on the risk-return relation have both been unified.

- Chapter 7: Efficient Diversification - The discussion of risk sharing, risk pooling, and time diversification has been extensively rewritten with a greater emphasis on intuition.

- Chapter 9: The Capital Asset Pricing Model - Added more discussion on extensions to the CAPM, in particular, the implications of labor and other nonfinancial income for the risk return trade-off.

- Chapter 10: Arbitrage Pricing Theory and Multifactor Models of Risk and Return - The chapter now contains an explicit illustration of the estimation and implementation of a multifactor security market line. It also contains a new section on smart betas.

- Chapter 11: The Efficient Market Hypothesis - Added more material on recently uncovered market anomalies, for example, related to volatility, accruals, growth, and profitability.

- Chapter 12: Behavioral Finance and Technical Analysis - Updated and expanded the material on the range of behavioral biases that seem to characterize investor decision making.

- Chapter 13: Empirical Evidence on Security Returns - Added a discussion of the debate concerning characteristics versus factor sensitivities as determinants of expected return.

- Chapter 24: Portfolio Performance Evaluation - Revamped the derivation and motivation of the M-square and T-square measures, which attempt to restate the Sharpe and Treynor measures in terms

Click here to view a sample chapter

About the authors

Zvi Bodie

Zvi Bodie is Professor Emeritus at Boston University. He holds a PhD from the Massachusetts Institute of Technology and has served on the finance faculty at the Harvard Business School and MIT’s Sloan School of Management.

Alex Kane

Alex Kane holds a PhD from the Stern School of Business of New York University and has been Visiting Professor at the Faculty of Economics, University of Tokyo; Graduate School of Business, Harvard; Kennedy School of Government, Harvard; and Research Associate, National Bureau of Economic Research.

Alan Marcus

Alan Marcus is the Mario J. Gabelli Professor of Finance in the Carroll School of Management at Boston College. He received his PhD in economics from MIT. Professor Marcus has been a visiting professor at the Athens Laboratory of Business Administration and at MIT’s Sloan School of Management.

Transform learning: boost grades, stimulate engagement and deliver an amazing course

Transform learning: boost grades, stimulate engagement and deliver an amazing course

Connect is an online platform integrating ready-made course content with assessment and tools. The platform uses the most established adaptive digital technology to deliver a more effective learning experience for both students and educators across over 90 disciplines.

Connect has changed the paradigm from students adapting to the classroom to education adapting to each student. Connect’s interactive technology provides each student with a tailored learning journey, enabling them to learn at their own pace and in their own way.

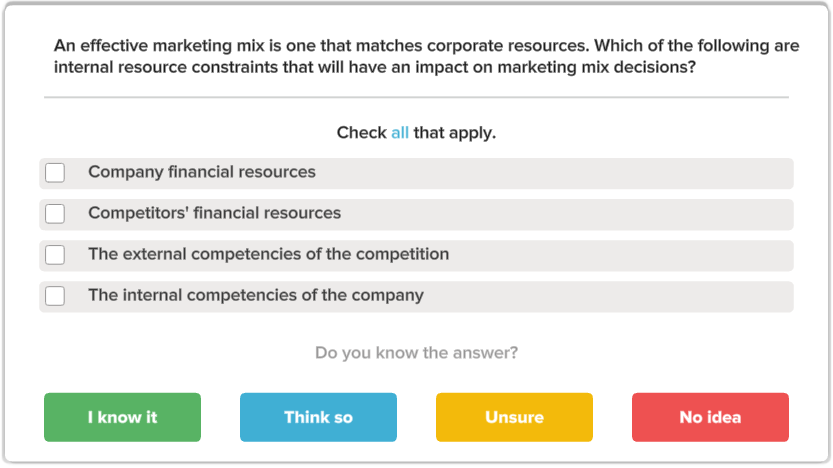

Connect’s integrated, adaptive SmartBook maximises learning by helping students study more efficiently, highlighting where in the chapter to focus, asking review questions, and pointing them to additional resources until they master the content.

Allows students to engage, visualize and interact with data in different ways whilst building their confidence.

Provide narrated and animated step-by-step walkthroughs of algorithmic versions of assigned problems, providing immediate feedback and showing students where they need to hone their skills.

Auto-graded algorithmic problems are also included offering students time to practice outside the classroom.

Request a review copy

To access your digital version of your Review Copy please complete the form below and we'll make the title available for you on our partner website - Vital Source.

Alternatively, our dedicated Academic Consultants, Digital Success and Customer Support teams are there to help you discover the right solution for your needs. We can create a bespoke offering that will allow you to achieve the institutional and commercial objectives of your learning & teaching programme.

Whether you want to adopt one of our titles or explore the use of our adaptive learning and teaching platforms, we will partner with you every step of the way to help ensure you unlock the potential of every student.

Simply complete this form to take your next step on your learning journey with McGraw-Hill Education.